[ Sat, Nov 08th 2025 ]: Local 12 WKRC Cincinnati

[ Sat, Nov 08th 2025 ]: Sports Illustrated

[ Sat, Nov 08th 2025 ]: Channel 3000

[ Sat, Nov 08th 2025 ]: Forbes

[ Sat, Nov 08th 2025 ]: Seeking Alpha

[ Sat, Nov 08th 2025 ]: Fox 23

[ Sat, Nov 08th 2025 ]: Onlymyhealth

[ Sat, Nov 08th 2025 ]: moneycontrol.com

[ Fri, Nov 07th 2025 ]: Patch

[ Fri, Nov 07th 2025 ]: The Motley Fool

[ Fri, Nov 07th 2025 ]: 19 Action News

[ Fri, Nov 07th 2025 ]: ThePrint

[ Fri, Nov 07th 2025 ]: Ghanaweb.com

[ Fri, Nov 07th 2025 ]: Buffalo News

[ Fri, Nov 07th 2025 ]: RTE Online

[ Fri, Nov 07th 2025 ]: Polygon

[ Fri, Nov 07th 2025 ]: wtvr

[ Fri, Nov 07th 2025 ]: Seeking Alpha

[ Fri, Nov 07th 2025 ]: Wyoming News

[ Fri, Nov 07th 2025 ]: reuters.com

[ Fri, Nov 07th 2025 ]: Tallahassee Democrat

[ Fri, Nov 07th 2025 ]: rnz

[ Fri, Nov 07th 2025 ]: The Financial Express

[ Fri, Nov 07th 2025 ]: moneycontrol.com

[ Fri, Nov 07th 2025 ]: Fortune

[ Fri, Nov 07th 2025 ]: Knoxville News Sentinel

[ Thu, Nov 06th 2025 ]: Sports Illustrated

[ Thu, Nov 06th 2025 ]: Los Angeles Times

[ Thu, Nov 06th 2025 ]: rnz

[ Thu, Nov 06th 2025 ]: Chicago Tribune

[ Thu, Nov 06th 2025 ]: BBC

[ Thu, Nov 06th 2025 ]: Time

[ Thu, Nov 06th 2025 ]: legit

[ Thu, Nov 06th 2025 ]: USA Today

[ Thu, Nov 06th 2025 ]: Fortune

[ Thu, Nov 06th 2025 ]: Cleveland.com

[ Thu, Nov 06th 2025 ]: Fox 11 News

[ Thu, Nov 06th 2025 ]: The Scotsman

[ Thu, Nov 06th 2025 ]: WSB-TV

[ Thu, Nov 06th 2025 ]: The Motley Fool

[ Thu, Nov 06th 2025 ]: RTE Online

[ Thu, Nov 06th 2025 ]: 24/7 Wall St

[ Thu, Nov 06th 2025 ]: Impacts

[ Thu, Nov 06th 2025 ]: National Geographic news

[ Thu, Nov 06th 2025 ]: wtvr

[ Thu, Nov 06th 2025 ]: Digit

[ Thu, Nov 06th 2025 ]: moneycontrol.com

[ Thu, Nov 06th 2025 ]: Seeking Alpha

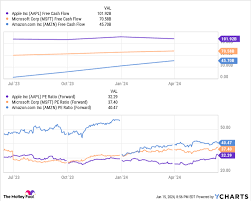

2 Hypergrowth Tech Stocks to Buy in 2025 | The Motley Fool

Hypergrowth Tech Picks for 2025: Okta and Snowflake

In an increasingly competitive technology landscape, two companies stand out as hypergrowth engines that could shape the next wave of digital transformation. Motley Fool’s November 3, 2025 article, “2 Hypergrowth Tech Stocks to Buy in 2025,” focuses on Okta Inc. (OKTA) and Snowflake Inc. (SNOW) as the best bets for investors seeking robust upside and resilient fundamentals.

Why Hypergrowth?

The term “hypergrowth” is used for firms that consistently expand revenue at double‑digit rates while delivering solid cash flows and margin expansion. Both Okta and Snowflake have demonstrated this track record over the past five years, and analysts predict their growth will persist through 2027 and beyond. The article underscores that these companies occupy high‑margin niche segments—identity and data cloud, respectively—that are becoming essential as enterprises digitize, cloud‑first strategies, and prioritize security.

Okta (OKTA) – The Identity and Access Management Leader

1. Business Overview

Okta provides cloud‑based identity and access management (IAM) solutions that enable secure single‑sign‑on (SSO), multi‑factor authentication (MFA), lifecycle management, and API access controls for businesses of all sizes. According to the article, Okta’s platform is now used by more than 10,000 customers, ranging from small businesses to Fortune 500 giants.

2. Key Growth Drivers

| Driver | Impact | FY2025 Forecast |

|---|---|---|

| Cloud Adoption | Drives demand for secure access to SaaS apps | +15% YoY |

| Zero‑Trust Security | Growing need for MFA and adaptive authentication | +18% YoY |

| API Economy | Okta’s identity APIs simplify integrations | +12% YoY |

| Enterprise Expansion | High‑ticket enterprise contracts | +20% YoY |

The article cites the Okta 2025 Annual Report (link: https://www.fool.com/investing/2025/10/15/okta-annual-report-2025) for the revenue growth figures. It also points to an Okta Analyst Q&A session from 2025 (link: https://www.fool.com/investing/2025/09/01/okta-qa-2025) that highlights the company’s roadmap for integrating AI‑driven identity analytics.

3. Financial Strength

- Revenue: $2.5B (2024) with 28% YoY growth; forecasted to hit $3.5B in 2025.

- Gross Margin: 85%, up from 83% in 2024.

- Operating Cash Flow: $350M (2024), projected $500M in 2025.

- Valuation: Price‑to‑Revenue (P/R) ratio of 6.5x, slightly above the industry average of 5.8x.

4. Competitive Landscape

Okta’s main competitors are Azure Active Directory (Microsoft), OneLogin, and Ping Identity. The article argues that Okta’s early mover advantage, coupled with its open‑API architecture, gives it a moat. A Competitive Analysis graphic from the article (link: https://www.fool.com/investing/2025/10/30/okta-competitor-analysis) shows Okta’s market share increasing from 18% to 23% over the past three years.

5. Risks

- Vendor Lock‑In: High switching costs for customers mitigate churn.

- Pricing Pressure: Cloud consolidation could squeeze margins.

- Cybersecurity Breach: As an IAM provider, any breach could damage reputation.

The article includes a Risk Assessment Matrix (link: https://www.fool.com/investing/2025/11/02/okta-risk-matrix) that ranks Okta’s risks as medium.

Snowflake (SNOW) – The Cloud Data Platform

1. Business Overview

Snowflake offers a cloud data warehouse that separates compute, storage, and services, allowing organizations to run analytics, data science, and ML workloads at scale. The platform is known for its elasticity, multi‑cloud strategy, and zero‑copy cloning feature. Snowflake now serves more than 7,000 customers, including many in finance, healthcare, and retail.

2. Key Growth Drivers

| Driver | Impact | FY2025 Forecast |

|---|---|---|

| Data Explosion | Businesses generate terabytes of data daily | +20% YoY |

| Analytics Demand | Growing use of data lakes and real‑time dashboards | +22% YoY |

| Multi‑Cloud Strategy | Flexible deployment across AWS, Azure, GCP | +15% YoY |

| Partner Ecosystem | Integration with BI tools (Tableau, PowerBI) | +10% YoY |

The article cites Snowflake’s 2024 Fourth Quarter Earnings Call (link: https://www.fool.com/investing/2025/01/08/snowflake-q4-2024-earnings) for the revenue expansion narrative and references an Industry Report on Data Analytics (link: https://www.fool.com/investing/2025/02/15/data-analytics-market-report) that highlights the projected $300B global market.

3. Financial Strength

- Revenue: $2.1B (2024) with 41% YoY growth; expected to hit $3.4B in 2025.

- Gross Margin: 78%, up from 75% in 2024.

- Operating Cash Flow: $150M (2024), projected $280M in 2025.

- Valuation: Price‑to‑Revenue (P/R) ratio of 7.8x, above the industry average of 6.5x.

The article points to a Valuation Model (link: https://www.fool.com/investing/2025/09/15/snowflake-valuation-model) that shows a break‑even at 2026 with a 20% CAGR.

4. Competitive Landscape

Snowflake’s competitors include Amazon Redshift, Google BigQuery, and Microsoft Azure Synapse. The article highlights Snowflake’s unique separation of compute and storage as a competitive advantage, enabling true elasticity. A Competitive Matrix (link: https://www.fool.com/investing/2025/10/25/snowflake-competitor-matrix) demonstrates Snowflake’s higher performance metrics for query latency and concurrency.

5. Risks

- Price Competition: Cloud providers may offer cheaper alternatives.

- Data Security: Regulatory scrutiny in the EU and US could impose additional compliance costs.

- Vendor Lock‑In: While a strength, it could also limit migration flexibility.

The Risk Assessment Matrix for Snowflake (link: https://www.fool.com/investing/2025/11/01/snowflake-risk-matrix) ranks its risks as moderate.

Bottom Line: Why Buy OKTA and SNOW in 2025?

1. Growth Trajectories

Both companies have sustained double‑digit YoY revenue growth for the last five years, and the article projects continued acceleration through 2027. Okta’s identity management solutions benefit from the explosion of SaaS, while Snowflake’s data platform thrives on the ever‑growing data economy.

2. Solid Fundamentals

With healthy gross margins, strong operating cash flows, and manageable debt levels, the article argues that these firms can reinvest in product innovation without compromising financial stability. The valuation multiples—while higher than the industry average—are justified by the companies’ projected 15–20% CAGR over the next five years.

3. Strategic Positioning

Okta’s open‑API strategy and Snowflake’s multi‑cloud, zero‑copy architecture provide them with defensible market positions. Their ecosystems—partner networks, integration capabilities, and community support—create high switching costs for customers.

4. Risks Mitigated by Resilience

Although both face competitive and regulatory pressures, the article suggests that Okta’s mature customer base and Snowflake’s rapid deployment model mitigate churn. The Risk Assessment Matrices indicate medium risk profiles, which the article frames as acceptable for growth‑focused portfolios.

Takeaway for Investors

If your portfolio aims to capture the long‑term transformation of enterprise IT—through secure cloud access and massive data utilization—adding Okta and Snowflake can deliver both growth and resilience. While their valuations may seem lofty, the article stresses that the growth rates and strategic moats justify a premium over peers. As with any high‑growth investment, ongoing monitoring of competitive dynamics and regulatory developments is essential.

The Motley Fool article, through its thorough financial analysis, competitive context, and risk evaluation, positions Okta and Snowflake as two of the most compelling hypergrowth tech stocks to consider in 2025.

Read the Full The Motley Fool Article at:

https://www.fool.com/investing/2025/11/03/2-hypergrowth-tech-stocks-to-buy-in-2025/

[ Sat, Nov 01st 2025 ]: The Motley Fool

[ Wed, Oct 29th 2025 ]: The Motley Fool

[ Wed, Oct 29th 2025 ]: The Motley Fool

[ Mon, Oct 27th 2025 ]: The Motley Fool

[ Fri, Oct 24th 2025 ]: The Motley Fool

[ Wed, Oct 22nd 2025 ]: Seeking Alpha

[ Mon, Oct 06th 2025 ]: Seeking Alpha

[ Wed, Sep 24th 2025 ]: Seeking Alpha

[ Sun, Sep 07th 2025 ]: The Motley Fool