Record-Breaking Roster Highlights Marquez Daniels' 1,200-Yard Season

Record-Breaking Roster Highlights Marquez Daniels' 1,200-Yard Season

RT E Launches 'Futureville': One-Hour Science Show for Irish Families During Science Week 2025

RT E Launches 'Futureville': One-Hour Science Show for Irish Families During Science Week 2025

Goochland County Unveils Technology Overlay District to Spark Tech Growth

Goochland County Unveils Technology Overlay District to Spark Tech Growth

Siga Q3 2025 Revenue Hits $14.6 M, Up 16% YoY

Siga Q3 2025 Revenue Hits $14.6 M, Up 16% YoY

Wyoming Science Teacher Turns Fair Projects into Step-by-Step Adventures

Wyoming Science Teacher Turns Fair Projects into Step-by-Step Adventures

Hungary Secures U.S. Nuclear Technology to Safely Store Spent Fuel

Hungary Secures U.S. Nuclear Technology to Safely Store Spent Fuel

TSC Announces 14th Annual Tallahassee Science Festival - 'Science in Every Corner' Theme

TSC Announces 14th Annual Tallahassee Science Festival - 'Science in Every Corner' Theme

Callaghan Innovation's Redundancies Cost Taxpayers Over NZ$10 Million

Callaghan Innovation's Redundancies Cost Taxpayers Over NZ$10 Million

Clean Science Ltd Reports Modest YoY Growth in Q3 FY24 - Net Sales Rise 2.72% to INR244.60 Crore

Clean Science Ltd Reports Modest YoY Growth in Q3 FY24 - Net Sales Rise 2.72% to INR244.60 Crore

Oak Ridge vs. Science Hill: Sweet 16 Clash Set for TSSAA Playoffs

Oak Ridge vs. Science Hill: Sweet 16 Clash Set for TSSAA Playoffs

The Best Current Premier League Forwards--Ranked

The Best Current Premier League Forwards--Ranked

Wall Street loses ground under the weight of falling technology stocks

Wall Street loses ground under the weight of falling technology stocks

Ranchers consider virtual fencing technology

Ranchers consider virtual fencing technology

Infectious disease research gets $75 million funding boost from government

Infectious disease research gets $75 million funding boost from government

Is breakfast really the most important meal of the day?

Is breakfast really the most important meal of the day?

8 Ways to Stay Healthy As You Age

8 Ways to Stay Healthy As You Age

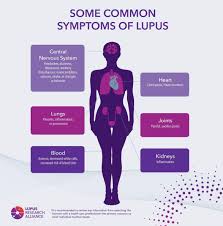

How a woman's journey with lupus reflects science's way of tackling the disease

How a woman's journey with lupus reflects science's way of tackling the disease

New AI technology helping with old hearing problem

New AI technology helping with old hearing problem

This author keeps predicting new 'dystopian' AI technology. What will come true next?

This author keeps predicting new 'dystopian' AI technology. What will come true next?

Mark Zuckerberg, Priscilla Chan shift philanthrop .. focus to how AI can accelerate science | Fortune

Mark Zuckerberg, Priscilla Chan shift philanthrop .. focus to how AI can accelerate science | Fortune

NY Man convicted for stealing US Technology and pitching it's military use to China

NY Man convicted for stealing US Technology and pitching it's military use to China

Security technology company to shutter Twinsburg facility, cut 240 jobs

Security technology company to shutter Twinsburg facility, cut 240 jobs

NY man convicted for stealing US technology and pitching its military use to China

NY man convicted for stealing US technology and pitching its military use to China

Think biowearable technology is just for athletes? Think again (aff)

Think biowearable technology is just for athletes? Think again (aff)

Zuckerberg, Chan shift bulk of philanthropy to science, focusing on AI and biology to curb disease

Zuckerberg, Chan shift bulk of philanthropy to science, focusing on AI and biology to curb disease

Array Technologies (ARRY) Q3 2025 Earnings Call Transcript | The Motley Fool

Array Technologies (ARRY) Q3 2025 Earnings Call Transcript | The Motley Fool

Curious Minds: Science Week 2025 Live for Primary Schools

Curious Minds: Science Week 2025 Live for Primary Schools

Deploying Agentic AI For SEO: A Playbook For Technology Leaders

Deploying Agentic AI For SEO: A Playbook For Technology Leaders

Is Bitmine Immersion Technologies (BMNR) Stock at $100 a Pipe Dream?

Is Bitmine Immersion Technologies (BMNR) Stock at $100 a Pipe Dream?

The Science Behind Dust: How Technology is Helping Decode the Hidden Health Risks in Our Homes

The Science Behind Dust: How Technology is Helping Decode the Hidden Health Risks in Our Homes

The science of why your body resists weight loss

The science of why your body resists weight loss

Start your career in business & information technology at Bryant & Stratton College

Start your career in business & information technology at Bryant & Stratton College

Alltech breaks ground on new crop science facility in Nicholasville

Alltech breaks ground on new crop science facility in Nicholasville

Science behind why humans stopped sleeping twice every night

Janus Henderson Global Life Sciences Fund Q3 2025 Portfolio Update

Science behind why humans stopped sleeping twice every night

Janus Henderson Global Life Sciences Fund Q3 2025 Portfolio Update

Manhattan University political science professor on the impact of the NYC mayoral election

Manhattan University political science professor on the impact of the NYC mayoral election

Some science and research investments protected, .. ents for colleges and universities in Budget 2025

Some science and research investments protected, .. ents for colleges and universities in Budget 2025

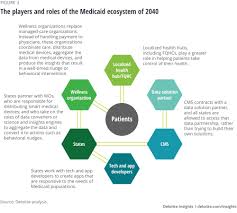

The Role Of Technology And Innovation In The Future Of Medicaid

The Role Of Technology And Innovation In The Future Of Medicaid

China is the new science power: How will Europe respond? - DW - 11/05/2025

China is the new science power: How will Europe respond? - DW - 11/05/2025

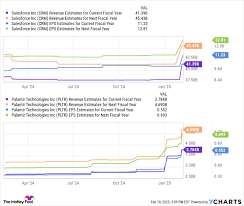

Array Technologies (ARRY) Q3 2025 Earnings Call Transcript | The Motley Fool

Array Technologies Q3 2025 Earnings Call: A Deep Dive into the Company’s Performance, Strategy, and Future Outlook

Array Technologies, the fabless semiconductor firm that designs AI‑centric chips for cloud and edge computing, held its third‑quarter 2025 earnings call on Wednesday, November 6, 2025. The company announced a solid financial performance, highlighted several key product launches, and outlined its growth strategy amid an increasingly competitive AI hardware landscape. Below is a comprehensive summary of the call, distilled from the transcript and related corporate releases.

1. Financial Highlights

Revenue & Margin Growth

- Q3 2025 revenue: $115 million, up 12 % YoY (up from $103 million in Q3 2024).

- Gross margin: 48 %, a modest improvement over the 45 % margin in the same quarter last year, driven by a higher mix of high‑margin “X‑Series” chips.

- Operating income: $12.4 million, compared to $9.1 million in Q3 2024, reflecting better cost discipline and improved gross margin.

- Net income: $9.8 million (Q3 2024: $6.6 million), translating to $0.18 EPS versus $0.12 EPS YoY.

Segment Performance

- Semiconductor Sales: $110 million, 96 % of total revenue. The segment saw a 13 % increase in unit sales, largely from cloud‑data‑center orders.

- Other Income: $5 million, consisting of consulting and licensing fees.

Capital & Cash Position

- Cash, cash equivalents, and marketable securities: $210 million at the end of Q3, up from $180 million at the end of Q2.

- Capital expenditures: $15 million on equipment and plant upgrades.

- Free cash flow: $8.2 million, a 24 % YoY increase.

2. Product Developments

“Array X” Series Launch

- Array Technologies announced the commercial availability of its flagship Array X chip, a next‑generation accelerator optimized for transformer‑based models.

- The X‑Series features a 12 nm process, 8 TB/s memory bandwidth, and 1.6 TFLOP/s compute, making it 30 % faster than the previous Array Z model.

- Initial orders from major cloud providers (Amazon Web Services, Microsoft Azure, and Google Cloud) indicate a strong uptake, with commitments for 3 TB of capacity in the next 12 months.

Edge‑Focused “Array Edge” Line

- The new Array Edge chips target autonomous vehicles and IoT gateways, featuring lower power consumption (<30 W) and real‑time inference capabilities.

- Array Technologies is partnering with NVIDIA for firmware integration and Bosch for automotive validation.

R&D Focus

- R&D expense rose to $18 million in Q3, a 25 % increase from Q3 2024, reflecting ongoing work on quantum‑aware AI and 3‑D integration technologies.

3. Market and Competitive Landscape

- The call’s CEO, David Chen, emphasized that the AI hardware market is expanding at >20 % CAGR, driven by demand for data‑center AI workloads and autonomous systems.

- Array’s primary competitors—NVIDIA, AMD, and Cerebras Systems—are investing heavily in high‑performance ASICs. Chen noted Array’s advantage in custom silicon density and energy efficiency.

- Supply chain constraints were acknowledged, but the company’s strategic supplier relationships and diversified fabs mitigated risks.

4. Operational Updates

Manufacturing and Supply Chain

- Array maintains manufacturing partnerships with TSMC (N7) and Samsung (N7), with an average 15‑month lead time for new fabs.

- The company is negotiating a long‑term contract with TSMC to secure priority slots for next‑gen 5 nm wafers.

Workforce & Talent

- Headcount increased to 1,250 employees (up from 1,120 at the end of Q2), with a focus on recruiting ASIC designers and AI software engineers.

ESG and Sustainability

- Array announced a new carbon‑neutral target by 2035, with initiatives to reduce manufacturing energy consumption by 15 % per silicon wafer.

5. Guidance for 2026

Revenue Outlook

- For FY 2026, Array expects $480 million in revenue, representing a 15 % CAGR.

- The company expects to maintain its gross margin in the 47‑49 % range.

Capital Expenditure

- FY 2026 capex is projected at $60 million, primarily for fab expansion and R&D infrastructure.

Product Pipeline

- The Array V processor (5 nm, 2.5 TFLOP/s) is slated for Q1 2027 release, targeting hyperscale data centers.

- A Quantum‑AI Co‑processor is in development, aimed at 2028.

6. Investor Q&A Highlights

- Capital Allocation – Chen confirmed that capital would be deployed to fund the next‑generation array lines and to accelerate R&D in AI acceleration and 3‑D packaging.

- Supply Chain Risks – While noting ongoing global semiconductor shortages, Array is actively diversifying suppliers and investing in inventory buffers.

- Competition – Array’s differentiation lies in specialized AI workloads, with a focus on performance-per-watt and integration flexibility.

- Financial Health – With a solid cash position and manageable debt load, Array can comfortably fund its growth plans without external financing.

7. Links and Additional Resources

The earnings call transcript references several corporate documents that provide deeper insight into Array’s operations:

- Array Technologies Q3 2025 Earnings Release (PDF). This release expands on the financial data, including detailed segment tables and footnote disclosures.

- Array X Product Brochure (PDF). Offers technical specifications and application notes for the new accelerator.

- Investor Relations – Press Release announcing the launch of the Array Edge line.

- ESG Report 2025 (PDF), summarizing Array’s sustainability initiatives and environmental impact metrics.

These documents corroborate the figures presented in the call and give investors a granular view of the company’s strategy.

8. Takeaway

Array Technologies delivered a robust Q3, achieving revenue growth, margin improvement, and a strong cash position. Its flagship Array X accelerator and the emerging Edge line demonstrate the company’s ability to innovate rapidly in response to the AI hardware market’s demands. While competition remains fierce and supply‑chain uncertainties persist, Array’s focused product strategy, diversified manufacturing base, and solid financial footing position it well for continued growth through 2026 and beyond.

Investors should note the company’s clear revenue and margin targets, its commitment to advancing next‑generation silicon, and its proactive stance on ESG issues. With its current momentum, Array Technologies appears poised to capitalize on the exploding demand for AI compute, making it a compelling watch for those invested in the semiconductor ecosystem.

Read the Full The Motley Fool Article at:

[ https://www.fool.com/earnings/call-transcripts/2025/11/06/array-technologies-arry-q3-2025-earnings-call-transcript/ ]

Zebra Technologies (ZBRA) Q3 2025 Earnings Call Transcript | The Motley Fool

The Smartest Technology Stock to Buy With $200 Right Now | The Motley Fool

Seagate Technology (STX) Q1 2026 Earnings Call Transcript | The Motley Fool

The Smartest Technology Stock to Buy With $200 Right Now | The Motley Fool

Seagate Technology (STX) Q1 2026 Earnings Call Transcript | The Motley Fool