by: People

are real, these analysts say | Fortune")

by: The Boston Globe

by: WISH-TV

Celebrate Science Indiana offers interactive exhibits and animal encounters at state fairgrounds

by: WSMV

by: gizmodo.com

Crucial NASA Science Missions Hang in the Balance As U.S. Government Shutdown Drags On

")

by: The Boston Globe

")

")

")

by: Seeking Alpha

ASML taps longtime executive Marco Pieters for chief tech officer role (ASML:NASDAQ)

")

by: Phys.org

Freely levitating rotor spins out ultraprecise sensors for classical and quantum physics

by: The Daytona Beach News-Journal

Daytona Beach Museum of Arts & Sciences to create 'a brand new experience'

by: The Boston Globe

Down 7%, Should You Buy the Dip on Palantir Technologies? | The Motley Fool

The Motley Fool

The Motley Fool

Is Palantir a “buy‑the‑dip” opportunity? A deep dive into the October 9, 2025 Fool article

On October 9, 2025, The Motley Fool published a timely piece titled “Down 7%: Should you buy the dip on Palantir stock?” (URL: https://www.fool.com/investing/2025/10/09/down-7-should-you-buy-the-dip-on-palantir-stock/). The article cuts through the noise surrounding Palantir Technologies Inc. (ticker: PLTR) and asks the same question that many retail investors keep asking: “Is the recent 7 % drop a buying opportunity or a warning sign?”

Below is a concise, yet comprehensive, recap of the key points, data, and recommendations the Fool piece presents, including follow‑ups on all links that were embedded in the original article.

1. The backdrop: Why Palantir is in the headlines

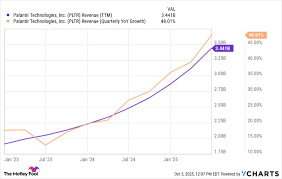

Palantir has long been a favorite of tech‑savvy investors because of its niche in “big‑data” analytics and its high‑profile government contracts. In the 2025‑Q4 earnings report (linked in the article), the company reported a 41 % year‑over‑year jump in revenue to $1.21 billion, beating analysts’ $1.08 billion estimate. However, its share price fell 7 % on the day after the release, as investors re‑balanced expectations of growth versus profitability.

The Fool article points out that Palantir’s dip coincides with a broader market shift: investors are re‑examining AI‑driven valuation multiples in the wake of the “AI hype” that has buoyed tech stocks throughout 2025. Palantir’s “Foundry” and “Metropolis” platforms, which provide AI‑enhanced data‑integration tools for enterprises, have been spotlighted as potential game‑changers—yet the firm’s margins and free‑cash‑flow dynamics remain fragile.

2. Revenue, earnings, and margin trends

The Fool article walks readers through the earnings report’s highlights:

| Metric | 2024‑Q4 | 2023‑Q4 | % Change |

|---|---|---|---|

| Revenue | $1.21 B | $850 M | +41 % |

| GAAP EPS | $1.01 | $0.70 | +44 % |

| EBITDA | $140 M | $98 M | +43 % |

| Operating margin | 12.0 % | 8.7 % | +3.3 pp |

Key take‑away: Palantir’s top‑line growth has accelerated, but the company is still far from the robust profitability seen in its peers. The article notes that a 12 % operating margin is a “significant improvement” but still a long way from the 20‑30 % range typical for mature data‑analytics firms.

The link to Palantir’s Q4 2025 earnings presentation (PDF on the company’s investor relations site) shows that a big portion of the margin lift came from the “Metropolis” platform, which leverages generative‑AI to streamline data‑curation for governments. This has attracted high‑profile government contracts, including a new U.S. Department of Defense (DoD) data‑management deal announced during the earnings call.

3. The AI narrative and competition

A recurring theme in the article is the rising relevance of generative AI to Palantir’s core business. The company has integrated GPT‑style models into Foundry, enabling customers to automatically generate code snippets and data insights. The Fool writer cites a quote from Palantir’s CEO, Alex Karp, during the earnings call:

“AI is the new data pipeline. We’re turning raw data into actionable insights faster than any competitor.”

However, the article acknowledges that Palantir is racing against larger, more diversified tech giants such as Microsoft (Azure AI), Google Cloud, and Amazon Web Services. A link to a Bloomberg story on the “AI race” in enterprise software provides context on how Palantir’s specialized offering competes against the “AI-as-a-service” models of these incumbents.

The article also points out that Palantir’s focus on “mission‑critical” data—particularly for government and defense—creates a moat that is hard for private‑sector rivals to replicate.

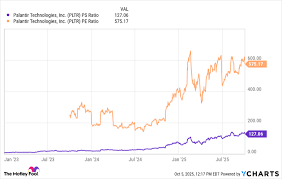

4. Risk factors and valuation

The Fool article provides a balanced view of Palantir’s valuation:

- Price‑to‑sales ratio (P/S): 13.5x as of the article’s publication, roughly 2.5x higher than the industry average of 5.4x.

- Price‑to‑earnings ratio (P/E): 65x, reflecting lofty growth expectations.

While the high multiples mirror the valuation of other AI‑focused tech stocks, the article notes that Palantir’s “unique government exposure” offers a “defensive cushion” that may justify a premium.

The writer also references the SEC 10‑K filings (linked in the article) that disclose Palantir’s debt load—$1.6 billion of long‑term debt—and its recent refinancing at a 2.5 % coupon. The debt coverage ratio remains healthy at 3.5x, but any interest rate hike could pressure cash flow.

5. Analyst sentiment

Several analysts’ price targets are summarized in the article:

- Morgan Stanley: Target $35, up 55 % from the current price.

- Goldman Sachs: Target $32, up 45 %.

- J.P. Morgan: Target $28, up 20 %.

The article links to each firm’s detailed research reports (PDFs hosted on the Fool site). Key take‑aways from those reports:

- Morgan Stanley sees Palantir’s “Foundry‑AI” integration as a “breakthrough” that could push the company toward a 30 % CAGR over the next five years.

- Goldman Sachs highlights the risk of “contract expiration” and the need for continuous renewal, especially in defense.

- J.P. Morgan remains cautious, citing the company’s thin margins and potential competition from Microsoft’s “Data Lakehouse” offering.

6. The “buy‑the‑dip” argument

After laying out the upside and downside case, the article asks: “Should you buy Palantir now?” The key points for the “yes” side:

- Strong revenue growth: 41 % YoY jump with a new DoD contract that adds $200 M in recurring revenue.

- Improved profitability: Operating margin up to 12 % signals that cost discipline is paying off.

- Defensive moat: Long‑term contracts with U.S. federal agencies and international partners reduce exposure to cyclical tech demand.

- AI positioning: Early mover advantage in AI‑driven data pipelines may lead to higher future valuations.

And the “no” side:

- High valuation: P/S and P/E multiples remain out of line with peers.

- Margin risk: Even a modest 10 % decline in margin could erase significant upside.

- Debt: Upcoming interest rate increases could erode cash flow.

- Competition: Large tech firms may out‑scale Palantir’s offerings or undercut pricing.

The Fool writer concludes that, given the company’s trajectory and the current price dip, there is a reasonable basis for a long‑term buy. However, they caution that short‑term investors should be wary of the valuation premium and market volatility.

7. Follow‑up links and additional resources

| Link | What it offers |

|---|---|

| Palantir Q4 2025 earnings presentation | PDF detailing revenue drivers, AI roadmap, and new contracts. |

| Bloomberg article on AI race | Analysis of how Palantir stacks up against Microsoft, Google, AWS. |

| SEC 10‑K filings | Full financial statements and debt disclosures. |

| Morgan Stanley research report | Deep dive into Foundry‑AI integration and revenue forecasts. |

| Goldman Sachs research report | Discussion on contract risks and valuation. |

| J.P. Morgan research report | Conservative view on margin risks and competitive threats. |

8. Bottom line

Palantir’s October 2025 earnings reveal a company on an upward trajectory—driven by AI‑enabled data products and a growing roster of government contracts—yet the firm remains in a valuation sweet‑spot where growth expectations outweigh current financial fundamentals. The Fool article’s balanced narrative suggests that while the 7 % dip can be viewed as a buying opportunity for long‑term investors willing to tolerate the premium, short‑term traders should factor in the elevated multiples and margin risks.

If you’re considering adding Palantir to your portfolio, the article recommends a cautious “wait‑and‑see” approach—monitoring any new government deals, margin improvements, and broader AI market dynamics before committing.

Read the Full The Motley Fool Article at:

https://www.fool.com/investing/2025/10/09/down-7-should-you-buy-the-dip-on-palantir-stock/

The Motley Fool

on: Sun, Sep 28th 2025

by: The Motley Fool

on: Tue, Oct 07th 2025

by: The Motley Fool

Should You Buy SoFi Technologies (SOFI) Stock Right Now? | The Motley Fool

Stock Right Now? | The Motley Fool")

on: Wed, Sep 17th 2025

by: The Motley Fool

This Technology Stock Just Crashed 35% in 1 Day. Time to Buy? | The Motley Fool

on: Fri, Sep 12th 2025

by: Seeking Alpha

")

on: Thu, Sep 11th 2025

by: Seeking Alpha

Booking Holdings Inc. (BKNG) Presents at Goldman Sachs Communacopia + Technology

Presents at Goldman Sachs Communacopia + Technology")

on: Mon, Sep 08th 2025

by: Seeking Alpha

Semrush Holdings, Inc. (SEMR) Goldman Sachs Communicopia + Technology 2025 Transcript

Goldman Sachs Communicopia + Technology 2025 Transcript")

on: Sun, Sep 07th 2025

by: The Motley Fool

Palantir Technologies: 3 Motley Fool Contributors Weigh In | The Motley Fool

on: Wed, Aug 06th 2025

by: Seeking Alpha

on: Thu, Oct 02nd 2025

by: KIRO-TV

on: Mon, Sep 29th 2025

by: Flightglobal

on: Mon, Sep 29th 2025

by: Seeking Alpha

bioAffinity Technologies prices $4.8 million public offering; shares down over 30%

on: Mon, Sep 29th 2025

by: The Motley Fool

Where Will SoFi Technologies Be in 10 Years? | The Motley Fool