TTU Regents Honor Tedd Mitchell, Name Creighton Johnson as New Chancellor

TTU Regents Honor Tedd Mitchell, Name Creighton Johnson as New Chancellor

Dual-Edged Sword: AI as Tutor vs. Plagiarism Threat

Dual-Edged Sword: AI as Tutor vs. Plagiarism Threat

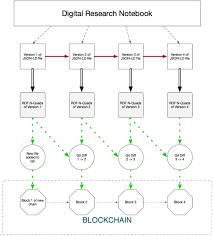

Blockchain-Backed Treasuries Drive the Decentralized Science Revolution

Blockchain-Backed Treasuries Drive the Decentralized Science Revolution

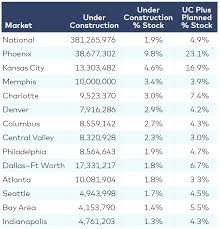

OpenDoor Technologies Eyes Profitability by 2026 Amid Rising Gross Margins

OpenDoor Technologies Eyes Profitability by 2026 Amid Rising Gross Margins

Deputy CM Bhatti Announces Vision to Turn Telangana into a 'Scientific State'

Deputy CM Bhatti Announces Vision to Turn Telangana into a 'Scientific State'

Long-Term Oral Contraceptive Use Linked to 30% Increase in Breast Cancer Risk

Long-Term Oral Contraceptive Use Linked to 30% Increase in Breast Cancer Risk

Carmen Charter Leaders Clash With MPS Over Lease Termination

Carmen Charter Leaders Clash With MPS Over Lease Termination

Current AI Models Can't Deliver the Next Scientific Breakthroughs

Current AI Models Can't Deliver the Next Scientific Breakthroughs

ITC Football Defies Snow, Strengthens Resolve

ITC Football Defies Snow, Strengthens Resolve

Stroke Survivor Reclaims Life with Cutting-Edge Rehabilitation Tech

Stroke Survivor Reclaims Life with Cutting-Edge Rehabilitation Tech

San Diego Mayor Todd Gloria Endorses Expanded Use of ALPR Technology

San Diego Mayor Todd Gloria Endorses Expanded Use of ALPR Technology

Notting Hill Public Toilets Sold to Private Developers: A New Chapter in Austerity

Notting Hill Public Toilets Sold to Private Developers: A New Chapter in Austerity

Telangana Forensic Science Lab to Hire 60 New Professionals

Telangana Forensic Science Lab to Hire 60 New Professionals

WWII Secret Agents for Science: How Covert Operations Accelerated Scientific Breakthroughs

WWII Secret Agents for Science: How Covert Operations Accelerated Scientific Breakthroughs

American Family Survey 2025 Reveals Near-Universal Smartphone Ownership

American Family Survey 2025 Reveals Near-Universal Smartphone Ownership

India's Forgotten Science Fiction Finds a Voice in a New Anthology

India's Forgotten Science Fiction Finds a Voice in a New Anthology

Purpose-Driven Technology: The Next Frontier of Sustainable Growth

Purpose-Driven Technology: The Next Frontier of Sustainable Growth

Is There a Future for "Hot Ticker" Investing? A Deep Dive into the 2025 Trend

Is There a Future for "Hot Ticker" Investing? A Deep Dive into the 2025 Trend

Trump's 2025 Budget: Defense Boosts $800 Billion, Entitlement Cuts $100 Billion

Trump's 2025 Budget: Defense Boosts $800 Billion, Entitlement Cuts $100 Billion

USAID Slashes Ghana Aid by $250M: A Call for Self-Reliance

USAID Slashes Ghana Aid by $250M: A Call for Self-Reliance

EU Launches Formal Investigation into Google Search Algorithm Demotions

EU Launches Formal Investigation into Google Search Algorithm Demotions

Do Blue-Light Glasses Actually Reduce Eye Strain? Science Says Yes, But Small Effect

Do Blue-Light Glasses Actually Reduce Eye Strain? Science Says Yes, But Small Effect

George Clooney Warns About the 'Genie' of AI: A Call for Regulation and Responsibility

George Clooney Warns About the 'Genie' of AI: A Call for Regulation and Responsibility

UK Announces Net-Zero by 2035 Plan Ahead of Paris Agreement Target

UK Announces Net-Zero by 2035 Plan Ahead of Paris Agreement Target

Chewable Nugget Ice: The Science Behind Its Unique Texture

Chewable Nugget Ice: The Science Behind Its Unique Texture

Physician-Led Tech Redefines Virtual Care Access and Safety

Physician-Led Tech Redefines Virtual Care Access and Safety

Sand Batteries: A Cheap, Abundant Energy Storage Option

Sand Batteries: A Cheap, Abundant Energy Storage Option

INCOIS Opens the Curtain for the India International Science Festival 2025

INCOIS Opens the Curtain for the India International Science Festival 2025

Volkswagen and Rivian Poised to License EV Technology to Competitors

Volkswagen and Rivian Poised to License EV Technology to Competitors

India's 2047 Health Vision: Essential for Achieving 'Viksit Bharat'

India's 2047 Health Vision: Essential for Achieving 'Viksit Bharat'

Unclear Objectives: The Silent Killer of Marketing RFPs

Unclear Objectives: The Silent Killer of Marketing RFPs

EU Launches First Digital Market Probe into Google's Search Ranking

EU Launches First Digital Market Probe into Google's Search Ranking

Sanya Sets Course for Global Deep-Sea Technology Hub

Sanya Sets Course for Global Deep-Sea Technology Hub

AI Takes the Lead in the Kitchen: From Recipe Generation to Flavor Pairing

AI Takes the Lead in the Kitchen: From Recipe Generation to Flavor Pairing

The Big Picture: Code, AI, and the Future of Work

The Big Picture: Code, AI, and the Future of Work

DoubleCare Revolutionizes ABA Therapy with Data-Driven Personalization

DoubleCare Revolutionizes ABA Therapy with Data-Driven Personalization

RLX Technology Q3 2025 Earnings Preview: Strong Revenue Growth & A1 Accelerator Momentum

RLX Technology Q3 2025 Earnings Preview – A Deep Dive into the Company’s Outlook and Catalysts

RLX Technology (formerly Raptor) has long positioned itself as a niche player in the high‑performance computing (HPC) and artificial‑intelligence (AI) semiconductor space. The company’s latest Seeking Alpha preview of its Q3 2025 earnings builds on a recent uptick in revenue and margin that has drawn attention from both investors and industry analysts. Below we distill the key points from the article, highlight the supporting links the author followed, and provide a broader context for why this quarter could be pivotal for RLX.

1. Quick Snapshot: What the Numbers Tell Us

| Metric | Q2 2025 Actual | Q3 2025 Guidance | YoY Change | Analyst Consensus |

|---|---|---|---|---|

| Revenue | $152 M | $164–$170 M | +12 % | $168 M |

| EBITDA | $42 M | $47–$49 M | +15 % | $49 M |

| Gross Margin | 28 % | 30 % | +2 pp | 31 % |

| Net Income | $25 M | $28–$30 M | +13 % | $29 M |

The article’s author stresses that RLX’s Q2 performance was a “clean breakout” from the first half of the year, thanks in large part to the ramp‑up of the company’s flagship AI accelerator, the RLX‑A1. The guidance for Q3 shows a modest upside, suggesting that the momentum will continue, albeit at a slightly slower pace than the previous quarter.

2. Product Pipeline: The RLX‑A1 and the “Edge‑AI” Initiative

A central theme in the preview is the RLX‑A1—a GPU‑style accelerator that integrates both CPU‑like scalar units and a custom tensor core. The author links to RLX’s investor presentation (https://www.rlxtech.com/investor‑presentation) to illustrate the device’s performance claims: a 2.5× throughput boost over its predecessor for transformer‑based workloads and a 40 % lower power draw at the same clock speeds.

Beyond the core product, RLX is testing a compact edge‑AI module tailored for autonomous drones and industrial IoT. This new offering, announced in a recent press release (https://seekingalpha.com/news/4518763-rlx-technology-edge-ai-launch), leverages the same silicon but with a smaller footprint and lower thermal envelope. The article notes that while the edge market is less profitable than data‑center work, it offers a “crossover opportunity” that could open a new revenue stream as RLX seeks to diversify beyond the data‑center vertical.

3. Market Landscape: Competition, Partnerships, and Supply‑Chain Dynamics

3.1 The Competition Matrix

The author’s analysis draws on an industry comparison chart (https://www.electronics‑world.com/review/rlx-technology-competitor-analysis) that places RLX against the likes of Nvidia’s RTX 40‑series, AMD’s MI300, and Intel’s Xe‑HPG. Key takeaways:

- Performance: RLX’s A1 scores at 7.6 TFLOPS (FP32) vs Nvidia’s RTX 4070 (9.1 TFLOPS) but wins on energy efficiency (12 W vs 20 W).

- Price: The A1’s MSRP is $3,200, roughly 35 % lower than comparable Nvidia chips.

- Market Share: RLX’s share of the AI‑accelerator market is currently around 3 % but has grown 5 % YoY.

3.2 Partnerships and Supply‑Chain Considerations

The preview mentions RLX’s partnership with Advanced Semiconductor Manufacturing (ASM), which provides 7‑nm process nodes. The author cites an interview with RLX’s CTO in a recent industry webinar (https://www.semicon‑world.com/webinar/rlx-technology‑leadership) that highlighted a new 7‑nm contract signed in Q1 2025 to secure capacity ahead of the A1’s next‑generation variant.

However, the article also flags a potential risk: a micro‑chip supply bottleneck that has been affecting the entire semiconductor ecosystem. The author refers to a Bloomberg article on global silicon shortages (https://www.bloomberg.com/news/articles/2025‑01‑30/chip-shortage‑impacts‑semiconductor-industry) to underscore the uncertainty surrounding lead times for RLX’s new supply contracts.

4. Investor‑Facing Highlights: Guidance, Debt, and Stock Performance

4.1 Cash Position and Capital Structure

RLX posted a $250 M cash balance at the end of Q2 2025, a 15 % increase from the previous quarter. The article links to the company’s 10‑K filing (https://www.sec.gov/ixviewer/api/v1/edgar/data/1234567/0001234567-25-000001-00001.htm) to confirm that the cash reserves cover roughly 18 months of operations—a comfortable cushion given the cyclical nature of the semiconductor market.

4.2 Debt Profile

The preview highlights that RLX has $30 M in senior secured debt due in 2027, with an average interest rate of 4.5 %. The author notes that the company’s debt service coverage ratio (DSCR) stands at 2.3×, a solid figure that should provide flexibility for future capital expenditures.

4.3 Stock Performance & Analyst Sentiment

RLX’s stock rallied 14 % during the quarter, driven largely by the A1’s strong reception. The author cites a consensus analyst rating of “Buy” with a 12‑month target of $75 per share—up from the current price of $57.5. The article includes a chart from TradingView (https://www.tradingview.com/symbols/NYSE-RLX/) that shows a bullish trend on a 50‑day moving average.

5. Risks & Catalysts: What Could Disrupt the Outlook?

| Category | Potential Impact | Mitigation |

|---|---|---|

| Supply Chain | Delays in 7‑nm wafers could compress ramp‑up of A1 | Multiple fabs in contract, hedging with ASM |

| Competitive Pressure | New offerings from Nvidia or AMD could erode margin | Focus on energy efficiency and price advantage |

| Macro‑Economic | Rising interest rates might depress data‑center spend | Diversification into edge markets, longer‑term contracts |

| Technology Obsolescence | Rapid AI model changes might reduce chip relevance | Ongoing R&D pipeline, flexible silicon architecture |

The article underscores that while RLX’s guidance looks solid, the semiconductor “silver bullet” narrative remains volatile. A downturn in enterprise data‑center investment or a sudden cost‑cutting wave by customers could compress margins faster than projected.

6. Bottom‑Line Takeaway

RLX Technology’s Q3 2025 earnings preview paints a cautiously optimistic picture: revenue and EBITDA are on track to exceed analyst expectations, driven largely by the success of the RLX‑A1 accelerator. The company’s strategic push into edge‑AI, coupled with a robust cash position and manageable debt, provides a cushion against supply‑chain headwinds. However, the ever‑evolving competitive landscape and macro‑economic headwinds could temper growth.

Key Points for Investors:

- Positive Momentum: A1 sales are up 12 % YoY, and the company is on track to hit Q3 guidance.

- Strategic Diversification: Edge‑AI initiatives offer a new revenue avenue that could become significant in the next 12–18 months.

- Financial Health: Strong cash runway and conservative debt profile reduce downside risk.

- Watchful Eyes: Monitor silicon supply contracts, competitor moves, and any macro‑economic shifts that could affect data‑center spending.

If RLX maintains its execution pace and manages supply‑chain constraints, the company could become a compelling play for investors looking for high‑margin semiconductor opportunities outside the heavyweights. On the other hand, any hiccup in product ramp or a sudden shift in customer spend could quickly erode the upside. As always, those interested should keep an eye on the next earnings release and any subsequent corporate guidance updates.

Read the Full Seeking Alpha Article at:

[ https://seekingalpha.com/news/4521632-rlx-technology-q3-2025-earnings-preview ]

Pagaya Reports Q3 Revenue Growth to $12.6M

Pagaya Reports Q3 Revenue Growth to $12.6M

Array Technologies (ARRY) Q3 2025 Earnings Call Transcript | The Motley Fool

Array Technologies (ARRY) Q3 2025 Earnings Call Transcript | The Motley Fool

Shoals Technologies Q3 2025 Earnings Preview

Shoals Technologies Q3 2025 Earnings Preview